Key Takeaways

- CalSavers is required for California businesses with 5+ employees that don’t already offer a qualified retirement plan. Employees are auto-enrolled at 5% contributions into Roth IRAs, but you’re not required to contribute anything as the employer.

- You might have better options than CalSavers. SIMPLE IRAs and SEP IRAs let employees save more, give you tax deductions for employer contributions, and help you stand out when recruiting and retaining talent.

- CalSavers has lower contribution limits. Employees can only save $7,000/year ($8,000 if 50+) in a Roth IRA through CalSavers, compared to $23,500 ($31,000 if 50+) in a 401(k).

- Employer-sponsored plans come with tax benefits. Your contributions to SIMPLE IRAs, SEP IRAs, or 401(k)s are tax-deductible, and you may qualify for federal tax credits up to $5,000/year for the first three years.

- This decision is about more than compliance. Offering a retirement plan with employer matching sends a message about how you value your team and can be more affordable than you think when you factor in tax benefits.

You opened the letter from the state, and there it is: your business needs to comply with CalSavers by a date that’s rapidly approaching. If you’re like most small business owners I talk with, you’re probably thinking, “What is this, and do I really have to do it?”

I get it. Running a small business is already a juggling act. You’re managing employees, serving customers, keeping the lights on, and somehow trying to stay profitable. And now the state is adding another requirement to your plate.

But here’s the thing. CalSavers isn’t just bureaucratic red tape. It’s California’s attempt to solve a real problem. And understanding your options now could save you headaches (and money) down the road.

Let’s break down what CalSavers actually is, who needs to comply, and whether it’s the right choice for your business. Because you might have better options than you think.

What CalSavers Is (And Why California Created It)

CalSavers is California’s state-mandated retirement savings program. It was created because millions of Californians (especially those working for small businesses) don’t have access to workplace retirement plans.

The statistics are pretty sobering. Nearly half of California’s private-sector workers don’t have a way to save for retirement through their job. And people without access to workplace retirement plans are 15 times less likely to save for retirement at all.

So the state stepped in. CalSavers is designed to make it easy for employees to start saving, even if their employer doesn’t want to (or can’t afford to) sponsor a traditional retirement plan.

Here’s how it works. Employees contribute to individual Roth IRA accounts through automatic payroll deductions. The money is theirs, even if they change jobs. And employers? You’re just facilitating the payroll deduction. You’re not contributing anything, and you’re not managing investments.

It’s a program that’s trying to help employees build financial security without putting a huge administrative burden on small business owners. That’s the theory, anyway.

Who Needs to Comply with CalSavers Requirements

So, does your business need to participate in CalSavers? Let’s figure that out.

The Basic Rule: If you’re a California employer with five or more employees and you don’t offer a qualified retirement plan, you’re required to register for CalSavers.

The Timeline: The mandate rolled out in phases based on business size:

- More than 100 employees: Had to register by June 30, 2020

- More than 50 employees: Had to register by June 30, 2021

- Five or more employees: Had to register by June 30, 2022

If you’re reading this in 2026 and you haven’t registered yet, you’re technically out of compliance. But don’t panic. California has been more focused on getting businesses registered than on collecting penalties. The key is to get compliant now.

What Happens If You Don’t Comply? The state can charge up to $250 per eligible employee if you fail to register. That can add up quickly if you have 10, 20, or 50 employees. But again, enforcement has been relatively light so far. The goal is participation, not punishment.

The Big Exemption: If your business already offers a qualified retirement plan (like a 401(k), SIMPLE IRA, or SEP IRA), you’re exempt from CalSavers. You just need to certify that you have a plan in place.

How CalSavers Works for Employers and Employees

Let’s talk about what actually happens if you register for CalSavers.

Automatic Enrollment: Your employees are automatically enrolled at a 5% contribution rate. They can adjust that rate or opt out completely, but the default is that they’re in.

Roth IRA Structure: Employee contributions go into individual Roth IRAs. That means they’re contributing after-tax dollars, and qualified withdrawals in retirement are tax-free.

Investment Options: CalSavers offers a simple lineup of target-date funds and a few other investment options. It’s not fancy, but it’s designed to be accessible for people who aren’t investment experts.

What It Costs You: As the employer, you’re not paying for investment management or account fees. But you do have some administrative responsibilities. You need to register, upload employee data, set up payroll deductions, and remit contributions on time.

For most small businesses, the process takes a few hours to set up. If you use a payroll provider (like Gusto, ADP, or Paychex), many of them have built-in CalSavers integration that makes it easier.

Employee Opt-Outs: Not every employee wants to participate. Some already have retirement savings elsewhere. Some prefer to manage their own finances. Employees can opt out at any time, and they’re not penalized for doing so.

The Pros and Cons of CalSavers for Small Business Owners

Now that you understand how CalSavers works, let’s talk about whether it’s actually a good option for your business.

The Benefits

Easy to Implement: Compared to setting up a 401(k) or other retirement plan, CalSavers is pretty straightforward. Registration takes a few hours, and if you use a payroll provider with CalSavers integration, the ongoing administration is minimal.

No Employer Contributions Required: You’re not on the hook for matching contributions or profit-sharing. Your only job is to facilitate the payroll deduction. This keeps costs low, which matters when you’re running a small business.

Helps Your Employees Start Saving: Even if you can’t afford to offer a traditional retirement plan with employer matching, CalSavers gives your team a way to build retirement savings. For some employees, this automatic enrollment might be the nudge they need to finally start saving.

Better Than Offering Nothing: If the alternative is that your employees have zero access to workplace retirement savings, CalSavers is a step in the right direction.

The Limitations

Less Flexibility Than Private Plans: CalSavers offers a limited investment menu. If you want more control over investment options or plan features, a private retirement plan gives you more choices.

No Employer Contribution Means No Tax Benefits for You: When you contribute to a 401(k) or SIMPLE IRA on behalf of your employees, those contributions are tax-deductible for your business. With CalSavers, there are no employer contributions, so you’re not getting any tax breaks.

Roth IRA Contribution Limits Are Lower: For 2026, employees can only contribute up to $7,000 per year to a Roth IRA ($8,000 if they’re 50 or older). Compare that to a 401(k), where the limit is $23,500 ($31,000 for those 50+). If you have high earners on your team, CalSavers won’t let them save as much as they might want to.

Missed Opportunity for Recruitment and Retention: Offering a retirement plan with employer matching is a competitive advantage when you’re trying to attract and keep great employees. CalSavers doesn’t differentiate you from other employers, because every California employee has access to it, whether their employer participates or not.

Alternatives to CalSavers: Other Retirement Plan Options

Here’s what a lot of small business owners don’t realize. Complying with CalSavers is the minimum requirement. But you have other options that might be better for your business and your team.

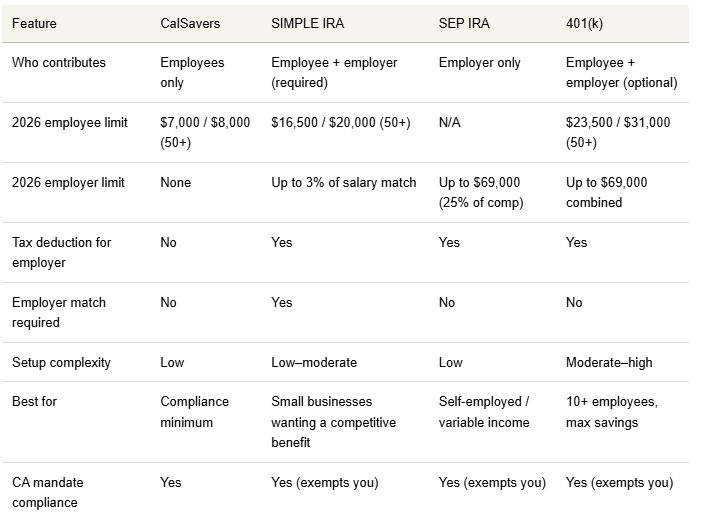

SIMPLE IRA

A SIMPLE IRA (Savings Incentive Match Plan for Employees) is one of the easiest employer-sponsored retirement plans to set up. You can offer it if you have 100 or fewer employees.

How it works: Employees can contribute up to $16,500 per year ($20,000 if they’re 50+), and you’re required to either match employee contributions dollar-for-dollar up to 3% of their salary, or contribute 2% of salary for all eligible employees regardless of whether they participate.

The upside? You get a tax deduction for your contributions, your employees can save significantly more than they could with CalSavers, and you’re offering a real benefit that helps with recruiting and retention.

SEP IRA

A SEP IRA (Simplified Employee Pension) is even simpler than a SIMPLE IRA. It’s an employer-only contribution plan, which means employees don’t contribute anything through payroll deductions.

You decide each year how much to contribute (up to 25% of compensation or $69,000 for 2026, whichever is less), and you have to contribute the same percentage for all eligible employees.

This works well if you want maximum flexibility year-to-year. In a profitable year, you can contribute generously. In a lean year, you can contribute less or nothing at all.

401(k) Plans

Traditional 401(k) plans offer the most flexibility and the highest contribution limits, but they also come with more administrative complexity and cost.

For businesses with at least 10 to 15 employees, a 401(k) can make sense. You can offer features like employer matching, profit-sharing, and Roth 401(k) options.

Safe Harbor 401(k) plans are a popular option for small businesses because they simplify compliance testing and allow owners to maximize their own contributions even if rank-and-file employees don’t participate much.

Which One Is Right for Your Business?

The answer depends on your goals, your budget, and your values as an employer.

If you’re bootstrapping and every dollar counts, CalSavers might be the right starting point.

But if you have the financial capacity to offer even a modest employer match (say, 3% through a SIMPLE IRA), that’s going to be far more valuable to your team than CalSavers alone. And the tax benefits to your business can make it more affordable than you think.

Next Steps for California Small Business Owners

Alright, so what should you actually do?

Step One: Determine If You’re Required to Participate

Count your employees. If you have five or more and you don’t offer a qualified retirement plan, you need to either register for CalSavers or set up your own plan.

Step Two: Decide If CalSavers Meets Your Goals

Ask yourself:

- Is CalSavers good enough, or do I want to offer something better?

- Can I afford to contribute to a SIMPLE IRA or SEP IRA?

- How important is offering competitive benefits for recruiting and retaining talent?

- What kind of employer do I want to be?

That last question matters more than you might think.

Step Three: Consider How Retirement Benefits Align with Your Values

If you see your business as just a way to generate income for yourself, then checking the CalSavers compliance box and moving on might make sense.

But if you see your team as partners in building something meaningful, investing in their financial future (even with a small employer match) sends a powerful message. It says, “I value you, and I want to help you build wealth, not just earn a paycheck.”

Step Four: Review the Financial Impact and Tax Benefits

Employer contributions to retirement plans are tax-deductible. There are also federal tax credits available for small businesses that start new retirement plans (up to $5,000 per year for the first three years, plus additional credits for employer contributions).

Run the numbers with your accountant or financial advisor. You might be surprised at how affordable a SIMPLE IRA or SEP IRA can be when you factor in the tax benefits.

Let’s Build a Retirement Strategy That Works for Your Business

Look, I get that CalSavers compliance feels like just another thing on your already too-long to-do list. And if you’re already stretched thin, the idea of setting up a whole retirement plan might seem overwhelming.

But here’s the truth. This decision isn’t just about compliance. It’s about what kind of company you want to build and how you want to take care of the people who help your business succeed.

If you’re not sure which direction to go, or if you want to explore whether a SIMPLE IRA, SEP IRA, or 401(k) makes sense for your business, let’s talk.

I work with small business owners across California, including clients in the San Francisco Bay Area, Sacramento, and Northern California, to design retirement plans that fit their budget, align with their values, and actually work for their team.

Schedule a consultation at wovencapital.net/schedule and we’ll walk through your specific situation. We can look at your business size, profitability, employee demographics, and long-term goals to figure out the best path forward.

Because at the end of the day, this isn’t just about checking a box. It’s about building a business that takes care of the people who make it possible.